Sponsored Ad: Click Here to Open a Share Trading Account Online for FREE and Pay ZERO Brokerage to Buy and Sell Shares!!!

There is a limit to invest your money in stock markets. Yes, ideally you should save 20-25% of your income and out of that 40% can be invested in stock markets.

Still, I do not advocate investing too much money in stock markets?

Let me give you an example.

Vijay’s take-home salary is 1 lakh a month.

– 25% saving is 25,000

– 40% of 25000 is 10,000

– In a year Vijay can invest 10,000*12 = 1,20,000 in stock markets which in other word is 10% of his take-home salary.

Assuming his salary is same for the next 30 years, or he invested Rs.1,20,000 for the next 30 years in stock markets and makes a return of 25% a year.

His invested money in 30 years = 120000 * 30 = 36,00,000 (36 Lakhs).

This is an investment that most can afford in 30 years, but the investment should not be made in one month or year – it should begin at a young age and by the time one needs money for financial goals like kids higher education in a foreign country or costly private colleges the money should be there.

At the end of 30 years, he would have Rs. 43,79,16,180.51 (Mind-boggling 43 crores+)

Total interest earned in the invested money of just 36 lakhs: Rs. 43,43,16,180.51 (Mind-boggling 43 crores+)

Can you see that almost all money Vijay gets back after 30 years is total money made from the stock markets? Assuming he started at 30, by the time he is 60 he will be richer than his own boss.

Today I got an email that I want to share with you.

Hi Dilip,

I have resumed work now (after coronavirus). Thanks for the promo of your new course. I only want to ask you is that whether potential revenues by way of referral commission from Demat accounts is enough to cover your costs or you have opened up this route recently and are testing the outcome? I will probably open a Demat a/c with Upstox and that I will map to you.

By the way, Nifty has today broken a modified Gann swing low (as per Marc Rivalland method) on 15-minute chart, at today opening. (14-10-2020).

Vivek

My reply was:

Vivek they pay me 30% of the brokerage generated. Yes, it’s less, but even 1 rupee is a rupee earned, right?

This is pure risk diversification (risk management is different). Me being conservative – not just in trading but in life – I cannot put too much money in stock markets even after knowing I am comparatively at par with some experts giving advice in moneycontrol or having Telegram channels of 50k people. This is risk management. I will pay a price if I do not follow. Actually, anyone will pay a price if they break the rules of risk management.

Nifty usually copies US markets, not technical. Tell me one reason – from 7600 to 12k in 4 months – where is economics? In fact, the virus is worst now and economics has not improved in the last 4 months. Nifty started to rise when US markets started to rise.

Thanks,

Dilip

Tip for those who trade directional future positional in Nifty: Read above – Nifty usually copies US markets. Try to copy what happened in US last trading day – with a stop loss half of the profits you want to take. Your success rate will be 70%.

What do you learn from my newsletters?

That be conservative in life – in spending as well as stock markets. The more you become conservative the more money will keep generating in your savings account and then route them in safe deposits like debt funds / FDs / Post Office savings etc. Keep a serious check. I write them down in an excel sheet every month. I assume less than 1% of earners do a simple thing as write down the savings and investments every month. It takes less than 15 minutes to do this check. Get alert if the savings go down by 10% in any month compared to the previous month. Check what mistake you did and never repeat the mistake again ever.

It is always advisable to keep 70% of your savings in guaranteed returns. Today the rate of Fixed Deposit is almost 6%. Yes, it’s less – but it’s not about money-making-money (even that’s good), but its more about saving for a better future and keeping the money safe with ZERO risk.

Here is Upstox link if you want to open an account mapped to me. If you are in 30% tax bracket, I suggest, to save taxes, open an account in your wife’s name. Learn to save money – there are many ways. This is one of them. Why pay 30% of the profits to the government when you can easily save it.

I will not name the broker, but you know that it does not allow selling deep out of the money option due to some reason – whatever – but with Upstox you can sell any option you want even if its 9% away – that’s guaranteed 1% a month. Please click on this link and open the account:

Of course, I will send a long term strategy combined with short term profit booking if you open an account mapped to me as a thank you gesture. It’s good if you don’t find time to trade options or futures and cannot monitor much the stock markets. It’s for investors who want to scale and are willing to wait for profits.

If you already have Upstox acc, you can learn the investing course by paying a small fee of 3500. You can click here and pay, (or pay by Google Pay to 9051143004). I will send you the course to your email for studying. If you have any doubts do ask me. Please note that its lifetime earning. You will lose only if you get stuck in a stock that keeps falling never to rise. But you will be doing this in 10+ stocks. Even if 2 fail – the rest will keep making money – in short term as well as long term. We will do scalping too in the stocks to take out small profits in between. You will learn everything.

Note that for stock investing there is no brokerage in Upstox too – so I make nothing if you just buy stocks. But that’s not important – what’s important is that you play safe and keep making over 20% return a year from stock markets. Start small then scale.

BTW, Ratan Tata has invested in Upstox. I am sure he must have done his research before putting his money there. He is a venture capitalist in Upstox – so he gets a share of profits every quarter.

Please take this email very seriously and become a conservative trader. I have many customers who want to trade with over 1 crore. I just fail to understand what’s the need? Have you ever asked yourself what will you do with that money? 1 crore needs to be saved first not to be traded.

If you can give good education to your kids and have more than 50 lakhs when you retire – that’s enough to live a peaceful retired life in India (as of 2020) unless of course, you plan to buy a Lamborghini when you retire. 😉

If you really have 1 crore spare, then keep at least 70% of it in safe deposits in 2-3 good rated debt fund. They make 1% more than FDs in the bank. Rest 30 lakh you can trade.

Hope you listen to me. If you have any question do ask.

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

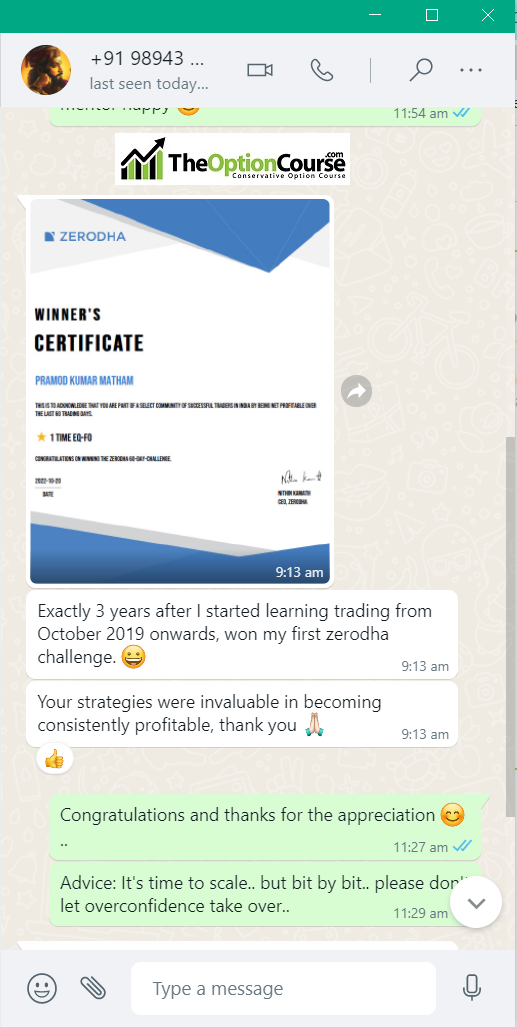

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users