Disclaimer: I DO NOT give tips or advisory services. This website is for educational purposes only. Full Disclaimer!!

This is a copy of my newsletter sent on 21-Nov-23 to my subscribers. If you want to register to receive my emails you can register in the newsletter form on this page.

=========================================================================

I received a lot of emails in reply to the email sent on 20-Nov-23. The text of that email was:

========================

Hi,

This is just a general question.

Have you planned for your retirement?

How much are you saving and where and what kinds of returns they are making?

Do you invest in NPS (National Pension System)?

Reply and I will try to help you plan your retirement. This will also help me to write a good article on what Indians are doing for retirement – the mistakes they are making and how they can improve.

Thanks,

Dilip

========================

Here are some of the emails I received.

Email 1:

Dear Dilip,

How are you?

I have only a PF (Provident Fund) for my retirement and to secure my family I have taken a Term Insurance Policy.

I am now 53, please let me know if any better can be done at this age, I know I am late but I have my valid reason, but still, I also understand very well that reasons will have no weight, ultimately we have to have money which has to be the ultimate result, this is the reason I took trading even though it’s known to be risky, please guide me.

Thank you

Regards,

Tony

Here is my reply to Toni:

53 is late – only 7 years to go for retirement.

Of course, you can take a private job till at least 65 years of age if health permits – then retire. This will help you to accumulate more money and be ready for retirement.

In the PF are you investing 1.5 Lakh a year (max limit)? If not please do it for the remaining time and try to extend it to 20 years for compounding to take effect. Real compounding will be in the last 5 years (15-20).

A term insurance policy is a good decision. Make sure to have at least 50 lakh term insurance.

You did not mention any health insurance. If you do not have one, then buy a health insurance policy for 5 lakh minimum for your family.

Once you retire take out all the money from your PF account and invest in a good short-term debt fund. These debt funds are safe and return 1% more than FDs.

In our old age, we must ensure that the money we made/got for retirement should be safe. Therefore I have recommended a debt fund and not an equity fund.

Redeem only what you need every month. This will become your pension.

Hope this helps.

Regards,

Dilip

==================================

Email 2:

Dear Dilip,

I have kept aside some money for retirement. Not sure if it is sufficient or not. Our family do not earn much. My wife is a homemaker.

For retirement, I have plans to do three things.

- Be a part of an NGO that looks after challenged girl children.

- Travel to at least one state in India every year.

- Make my home in such a way that my Children and Grandchildren will love to visit at least once a year if they are not staying with me.

I do not have NPS (National Pension System) since I am an NRI.

The above are answers to the specific questions.

Regards,

Sony

My reply to Sony:

Sony as far as I know NRIs earn very well.

In any case, you can start investing whatever you can save.

If you do not know Non-Resident Indians (NRIs) aged 18 to 60 can invest in India’s National Pension Scheme (NPS) by adhering to KYC norms. The NRIs can make contributions to NPS from their NRO/NRE account.

If you do not have an NRO / NRE account kindly open one and start investing in NPS as soon as possible.

Regards,

Dilip

Note on NRO (Non-Resident Ordinary)/ NRE (Non-Resident (External)) Accounts

This table will help you to know the difference in these accounts:

Email 3:

Dear Sir,

I retired already a couple of years back. Planning was done while I was in service.

Regards,

Gautam

My reply to Gautam:

Thats good.

Do you get a pension?

Regards,

Dilip

I have still not received a reply from him but I guess since he was in some service he must be getting a pension. Or his company must have paid him a gratuity.

What is gratuity? Gratuity is an amount paid by an employer to its employees for rendering their services for equal to or more than 5 years. Gratuity is paid to an employee as part of his/her salary and is considered to be a benefit plan which is designed to help the employee during his/her retirement.

Please note that a Gratuity is paid 100% by the employer to the employee. There is no contribution required from the employee during the term of the service.

If you are also in service and your company has a gratuity program then my advice is that do not avail Voluntary Retirement Scheme (VRS) if you will miss out on gratuity. Some people retire early to get a higher-paying job. But you must do calculations of what you will miss if you retire early before deciding to retire.

===================================

Email 4:

Hi Dilip ji

Not yet…

Sachin Aggarwal

This email surprised me as Mr. Sachin has still not planned for retirement. Retirement and investment planning should be started from the day you get your first salary. The earlier you invest the greater will be returns. If you plan well early for retirement you can retire before the age of retirement.

So I replied to him, “What’s your age and why you have not started to plan for retirement?”

Regards,

Dilip

Awaiting his reply.

=============================

Email 5:

Sir, so far I have not planned for retirement.

Saving in FD, SIP.

I am 25 and want to retire by 45, working in a PSU bank as a clerk.

No investment in NPS (National Pension System) so far.

Thanks and regards,

Anjana

Here is my reply to Anjana:

>> Saving in FD, SIP

Continue and also invest in PPF. It can be opened in any SBI Branch.

Regards,

Dilip

=============================

Email 6:

Hi Dilip,

I have been actively concerned and investing for retirement from 2016 onwards. The plan was to at least build a 30X corpus of inflation-adjusted current expenses. For that, investing in index mutual funds (Nifty 50, Next 50, Midcap and Small Cap index) 1X of current expense in equity: debt ratio of 80:20 plus EPF (Employees’ Provident Fund).

Still, I am doubtful of achieving the goal. So the plan is to increase the investment by 10% every year.

Start a PPF (Public Provident Fund Account) as well.

Jijesh Janardhanan

Here is my reply to Jijesh:

Continue the other investments – do not break the SIP if the market falls.

Regards,

Dilip

His reply:

Yes PPF is also there, since the interest rates are low, I have stopped in between. Now whenever doing equity: debt rebalancing, will add to PPF (max 1.5L / year).

SIP is continuing.

Jijesh Janardhanan

=================================

I have given you a lot of advice in this post on how you should plan for retirement and why it is important to start as early as possible for compounding to take effect so that you can retire peacefully.

Hope you will start planning for your retirement soon.

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

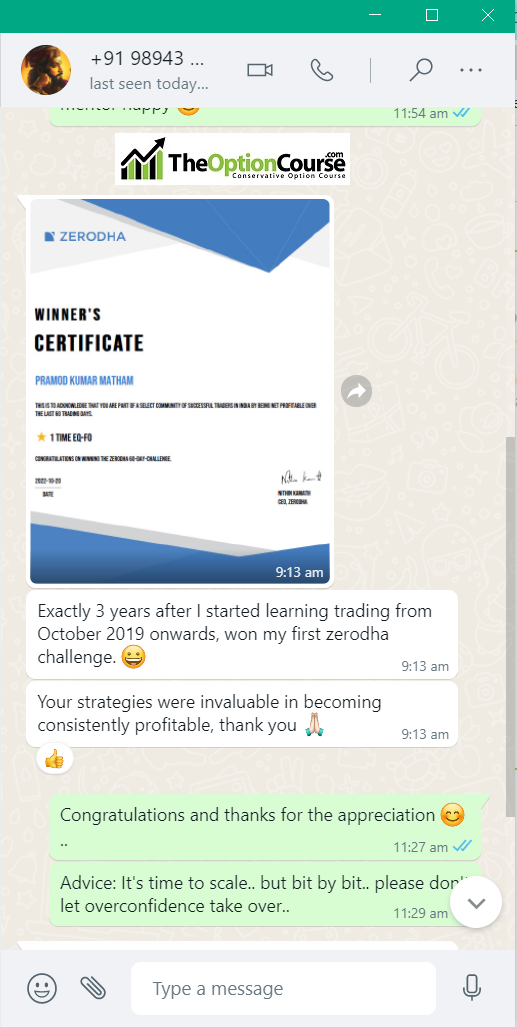

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users