Well yesterday I got an email which was very disturbing. Someone lost more than Rs. 2 crores trading options.

Click on the image below to enlarge and read the email properly.

Rs 2 Crore Loss – Click to Enlarge

Disclaimer: I cannot verify the authenticity of this email nor do I know whether it is true or not, but if it is, then probably this is something un-explainable and inexcusable.

I mean you cannot lose so much money that can change your life. 5-7 lakhs is ok. In the long run it won’t matter much, it will not change your life. But that is it.

Here is another trader who lost more than Rs. 40 lakhs.

If you have lost more than a lakh in the stock market, you should stop trading and learn trading – not just keep speculating and losing. Most of the traders who lose money are option buyers.

Read this article to know why option buyers never make money over a period of time. By the way selling naked options is even more dangerous.

Just imagine what this person could have done with this money or anyone of us can do with so much money especially in India. I mean you need not work for the rest of your life and still generate enough money every month from guaranteed returns that you would find hard to finish even if you live a lavish lifestyle.

If he bought a big house in any city of his choice, and a great car for 1 crore (85-90 lakhs for the house and 10-15 lakhs for the car. I know car lovers will hate me for this but in economics the car has a diminishing return – the house can be sold at a profit 🙂 ) – he would still be left with Rs. 1 crore. If he goes and fix this in a bank – he makes Rs. 72,588.00 per month from interests alone (calculated at current Bank Fixed Deposit (FD) of 8.75% per year).

Better still if he keeps this in a debt/liquid fund which returns better than Bank FDs, then he makes even more. Currently debt funds in India are making more than 10% a year – but it keeps changing and is not guaranteed “on paper”. However they return better than bank fixed deposits.

Whats more, if he can somehow keep that money in the debt fund for three years – then the tax on the returns gets highly reduced. You only pay 20% of the profits after indexation. Bank FDs returns are taxed as per your income slab even if it is kept for 5 years.

He can always invest 50% in bank fixed deposits and 50% in liquid funds to diversify the risk. Click here to read how I manage my financial portfolio and diversify my risk.

He can spend the money earned from interests guilt free, as he likes, without saving one rupee from it as he will again get 72,588.00 (or more if 50% of it is in liquid fund) next month. 🙂 Even after spending this much money, he gets to keep Rs. 1 crore. What a loss.

Here are some more loss stories that I was told on phone or email. All personal details of the trader is kept confidential:

I know one person who did not take a stop loss even when his losses were at almost one crore. He had sold too many naked Nifty Futures when Nifty was rising in 2013-14 thinking it will come down. This was when Nifty was at 7700. I asked him to take a stop loss immediately but he did not. Today Nifty is nearing 9000, if he has not taken a stop loss imagine where his losses are today. This in a small city in Warangal – Andhra Pradesh.

At least five traders have told me their losses have exceeded 40 lakhs. One person sold his property worth lakhs and lost all his money trading intraday.

An engineer left a plum job of software engineer in Bangalore to do trading full time. Initially made a lot of money, got greedy and lost it all. Now he is asking his friends to look a job for him.

Here is another sad story from Goa:

Dear Sir,

My name is XXX, I’m from Goa, I have been a trader for almost 4-5 years with little breaks in between. But, I have never made any mentionable profits as such. Mostly it was like little profit, more loss, this cycle was repeated for quite some time, till my account eroded considerably.

Furthermore I had taken money from my friends and colleagues and lost it too (approx. 15 lakhs) now these people are behind me to pay back their money, making my life really miserable.

I used to trade mostly in Nifty Futures (Index Futures – most of the times I used to make profits) and Nifty Options (Index Options – always made losses, unless some fluke trade made me profit).

Now, my situation is so bad, that even my wife and parents are not so free to speak to me. They have become reluctant to even talk to me normal day to day talking, because they have come to know what I have done with my money and my friends money. My friends frequently call me on my phone and visit my home and threaten me. Now the situation has become unbearable.

Even my self confidence has gone so low, I hardly go out of the home, even if I have to go for some urgent work, I wear full face black helmet and go, to avoid the people from whom I had taken money. To make matters worse, I’m not even getting a job with justifiable salary in Goa (this is because of the break I took to do full time trading).

It has become difficult for me to meet my daily expenses, and I can’t support my family.

Sir, right now I have only 16 thousand rupees left in my trading account, and don’t have money to pay you fully for the course, but I can pay you Rs. 2,000/- now and Rs. 2,000/- after some days, when I start making profits with the Rs. 16,000 that I have in my trading account and taking support of your options course.

So, I request your good self to kindly bear with me and allow me to do the course with 2,000 now and balance 2,000 later. But one thing is sure that I will definitely pay your money, since you are my Guru.

Please help me Sir, I will be really grateful to you.

I asked him to look for a job and stop trading.

Another email:

I have been trading unsuccessfully since 10 years, meaning I keep changing strategies. I have a good understanding on trends, position sizing, supply and demand, however, when it comes to put on the trade, I am not consistent. The reason being I think directional trading can change your view with market ongoing. I also studied in depth options and have a good understanding on payoff, risk:reward, etc on option trading for iron condors, butterfly, credit spreads, etc.

What was difficult is that risk : reward are really risky when we see the actual options on NSE. i.e. you get less credit versus the risk. Sometimes it is skewed to 1:5 R:R. So if I think to earn Rs. 10,000 profit, I need to put on risk of Rs. 50,000. If the R:R is so extreme, I think 2 or 3 losses out of 10 will keep trading account in negative zone.

My view: 10 years of trading and still losing. Even worse he learned nothing. In 10 years a kid who was in class 1 will be appearing for his 10th board exams with a lot of knowledge about the world. What a waste of time. Money can be earned again, time will NEVER come back. To me time is more important than money.

This is what I replied: You may be right in what you say BUT only when you DO NOT manage risk well before time AND you have NOT hedged your positions.

Options can be made to play against one another.

Why let that 1 loss exceed the limit? Managing it before is the key and playing it smartly is also important.

There are countless stories I hear almost everyday but they are not worth mentioning. Please stop your trading if you are still losing money trading options. Read books or good websites online on options. I bet if you keep speculating, you keep losing.

Cheer up. There are some good stories as well. Someone told me that two guys in his city were making almost 5 lakhs every month trading options with a 40 lakh account. That is over 12% return a month. 🙂 Well congratulations if this is true.

So making money is possible but if you have some knowledge and have a strict plan. Enhance your knowledge in options and then trade. Please do not speculate. You will only lose money, and it will slowly accumulate to lakhs. Do not let yourself bleed slowly – you will not realize the small losses, but by the time you realize you may be deep in losses.

How much money have you lost or made trading options? Please do write in comment. Your email will not be shown and you can always use your first name to hide your identity. Thanks.

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

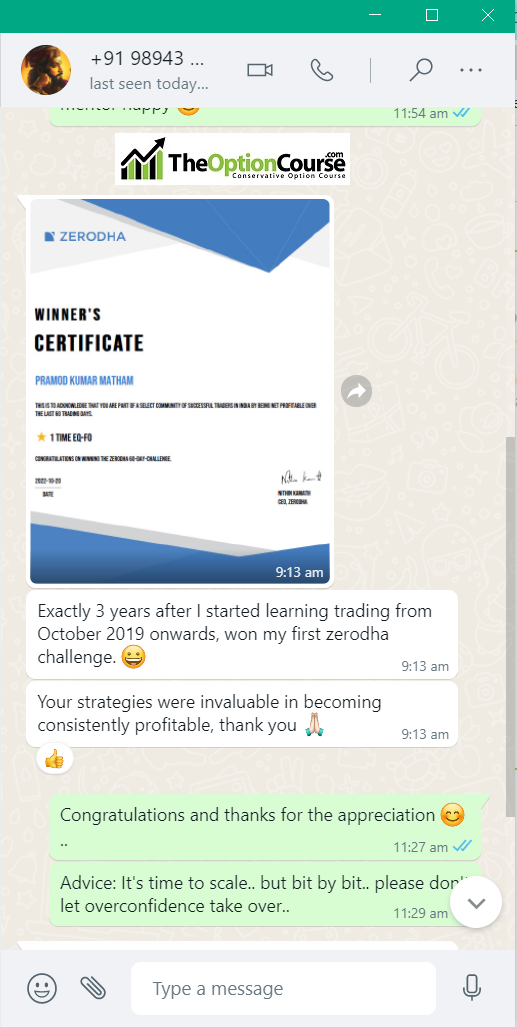

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Comments on this entry are closed.

i have made net profit of 3k in jan. till now i have lost around 5k. right now i have holding in which i have not booked loss. but i have purchased union bank in which i have 7k loss. i m holding this. i m trading into equity cash. also in l & t finance i have current loss of 1k but not booked loss i am waiting.

Poonam,

You are doing a good job. Trading slowly and small. There will be some volatility in your account – so please do not bother about these ups and downs.

However I would like to know was there any basis on which you had chosen to invest in Union Bank and L&T Finance? Did your broker asked you to buy it?

Tip for everyone reading this: Do not fall for stock buying advice from your broker – they want you to trade and that’s it. They are least bothered whether you make money or not. If you trade in profit or loss – they always make money. So please do your own research before investing in any stock.

There are much better and safer stocks in banking space. Like ICICI Bank, Axis Bank, HDFC Bank, SBI etc. L&T Finance is ok, its a big name but Union Bank is a weak mid cap very volatile counter. These shares never recover for years or jump 20% any day – we do not know. So you should not invest in such stocks.

Tip:

1. If Union Bank is more than 10% down from your holding’s average price – consider averaging it out. But do not keep averaging – only put that much money in a stock where you feel comfortable. You may not be able to get out from this stock soon so you should average it up to a limit.

2. If you find a better opportunity – a better stock at a better price – consider taking a loss in Union Bank and get into another better stock. But please do your research before taking the loss.

Looks like you are very young. Start accumulating Group A stocks (Large Caps only) whenever there is a fall. Buy a small amount every month. I guarantee if you do so, within years your account will show amazing returns.

Dilip Sir…..

Since Jul 2014 total loss is 25000/-(Margin Intraday )

But after 26 Dec 14….total profit 8000 /- (Option buying naked ) (Sorry Dilip Sir for this 🙂 till today..

Thank You Dilip Sir. God bless You.:)

Abhishek,

25k loss is very small and I am happy that you are now trying to control greed and trading conservatively. You are young and have enough time to accumulate wealth through stock markets. Learn as much as you can and trade conservatively.

Thanks for being a regular visitor.

God Bless!

Firstly, I would like to commend you on your consistency and good work. Your blog and advice is really a gem and a goldmine for Indian traders.

Secondly, about your reference to debt funds in the article, does this include Fixed Maturity Plans (FMPs) too?

I tend to keep away from debt investments because the taxation part was confusing and not as straightforward as equity. Are there any tax-efficient debt mutual funds you can recommend?

Thank you 🙂

Hi Mr. Nathan,

Thanks for your kind words. This keeps me motivated. 🙂

>> Your reference to debt funds in the article, does this include Fixed Maturity Plans (FMPs) too?

Fixed Maturity Plans or FMPs are also debt funds but are locked-in for a period of time. Minimum is 1 month. Most FMPs now days come with 3-years lock in period because of the long term capital gain taxation benefit. Both debt funds and FMPs are taxed in the same way.

If you keep money in debt/liquid or Fixed Maturity Plan funds for 3 years indexation comes into effect.

Real profit is eaten away by inflation. So the Government of India declares the inflation rate every year. FMP or debt fund is in profit only if it made more than the inflation that year. For example lets say all three years the inflation was 8% and the FMP returned 10%. Which means real profit is only 2%. So you will have to pay a tax of 20% on the profit made after taking into account the inflation. Thus the tax liability will get reduced to large extend. If both the FMP return rate and inflation rate were same you do not pay any tax.

As you can see FMPs offer better post-tax returns than FDs. Profit from FDs for any amount of time will be added to your income and taxed accordingly in that year.

For both debt and FMPs – if they are kept for less than 3 years short term capital gains comes into effect and the profit is included in your income and taxed as per your income slab, just like FDs.

In equity – if you sell an equity share for profit within 1 year you will have to pay 15% of the profit as tax whatever slab you are in. If you sell it after holding it for more than 1 year then the profits are absolutely tax free.

This is done by Government of India to encourage retail traders to participate in the stock exchange and hold the stocks for a period longer than 1 year. Also there is a big chance that a good company’s stock will be in profit in about a year, though in reality we do not know.

Further if people hold the stock for 1 year then demand will increase as sellers will get reduced. This will increase the price of the stock. 🙂 This also helps to reduce the volatility in markets.

Any dividends from either the shares or the debt funds or FMPs are tax free as the dividends are paid only after paying taxes to the government. Any profit cannot be doubled taxed.

I hope Mr. Nathan now your doubts are cleared about the taxation part on the debt funds.

I encourage everyone reading this to invest at least some money every month in quality debt funds. Maybe one day I will write about how to chose good debt funds.

>> Are there any tax-efficient debt mutual funds you can recommend?

The best way to save tax and make money from the stock market is to invest in ELSS (Equity Linked Savings Scheme) Mutual Funds through the Systematic Investment Plan (SIP) method. In SIP the investor invests a fixed amount every month in a mutual fund. This is done automatically.

These are funds enable investors to avail tax rebates under Section 80-C of the Income Tax Act.

You can chose a top ELSS fund from here:

http://www.moneycontrol.com/mutual-funds/performance-tracker/returns/elss.html

If you insist on investing in debt funds only for tax saving purpose, I encourage to invest in debt funds as in FMPs you cannot take money out if required before the lock-in period. Here is the link to know the returns of debt funds:

http://www.moneycontrol.com/mutual-funds/performance-tracker/returns/debt-long-term.html

Thank you once again for asking this question and for your kind words.

Disclaimer: I am not a tax expert. Please consult a tax professional before filing your income tax returns.

Thank you for the crystal clear explanation. I looked into your article about managing financial portfolio risk while trading and agree with the 25-25-25-25 rule.

If people followed it in letter and spirit, there wouldn’t be such horror stories as 2 crores loss or 40 lakhs loss (not sure if that loss figure refers to trade turnover rather than actual capital… but either way, it’s a mind-boggling gamble).

Overall, risk management is always better than giving in to the fluctuations of fear and greed. This psychology should take precedence irrespective of whether we’re in a bull run or a bear market.

I had a share trading account. I got it in early 2007. I lost 15 lks money in trading , cash and F&O ,

Please send me how to trade in options.

Thanks Dilip. You are doing really good job, you are not just experiencing the trading but sharing that. Sharing bad experiences. Also educating others to earn money.

I lost arount 200k in last two motnhe. was thinking to turn full time trader, but NOT NOW. I will not do mistakes done by others, big thank to you.

I will go through your trainings and start earning slowly, and small profits will make big money…

thank you,

So Happy that you got the point. Yes it is small boring profits that can have a huge impact later in our life. There is no trade in this world that can make to rich in a day, or a month or even a year – it will take years before you actually make a lot of money trading. 10 years is good enough – frankly 10 years is NOT too big a time but people unfortunately get want to rich today. To make huge profits people keep losing for more than a decade. Nice to see people are learning from the post.

Good, sir ji

I lost 72 lakhs

i have been trading from 10 years all savings gone trading is very addictive so i advice to avoid trading if u r loosing consistently without any change

sometimes it is very hard to stop but u need to do it otherwise life will be miserable

Correct Venkat. I lost 10% of what you have in 2007-08 but it still pains though I have recovered. What worked in my favour is that I started paper trading with a 10 lakh account. Paper trading helps a lot to fight the real war. My advice for you is to now stop trading and keep investing in index funds.