Disclaimer: I DO NOT give tips or advisory services. This website is for educational purposes only. Full Disclaimer!!

People all over the world do absolutely no planning on how much to invest in stock markets. They just keep investing on gut feelings, as much as possible, to recover losses. This is a poor money management skill. In this article I will help you learn how to properly plan investing in stock markets. This post will help you a lot to plan your investments in future in stock markets, especially if you are young.

Contrary to traditional belief, you do not need too much money to start investing in stock markets but you must know where to invest. In fact it is very important for a beginner not to invest too much money at the very beginning. It is important that you separate the cash that you want to invest in stock markets from what is needed to live a life. Never take a risk with the money you cannot afford to lose.

As a thumb rule, not more than 10-15% of your salary should be invested in stock markets. Which means if your take-home salary is Rs. 50,000/-, then at max invest 5000 – 7500 per month in stock markets.

This can be done for 24 months. Which means once your investment in the stock market equals two years of your salary – you should stop investing in stock markets unless you start making profits.

In other words, if you invested for 2 years in stock markets, 10-15% of your salary then at the end of 2 years if:

a) You are making losses – stop investing any more money in stock markets – educate yourself – start paper trading.

b) You are making profits – you can keep investing up to 20% of your salary in stock markets – but up to the next 10 years only.

Here is some calculation. Ram’s salary is 50,000 pm. He starts investing 10% of it in stock markets for 2 years.

5000*2*12 = Rs. 1,20,000 invested. He is making profits. How much here is not important – what is important is that he is making profits.

He now decides to invest 15% of his salary in stock markets for the next 3 years. His salary now is 60,000.

9000*3*12 = Rs. 3,24,000 invested.

Since he is still making profits he decides to invest 20% of his take-home salary which is 75,000 per month now, for the remaining 5 years.

15000*5*12 = Rs. 9,00,000 invested.

Total invested till now in 10 years: 1,20,000+3,24,000+9,00,000 = Rs. 13,44,000/-

That’s it, he decided to control his greed and stop investing in stock markets. He will from now on invest in fixed deposit schemes in banks, liquid funds and post office schemes.

What you read above is proper money management.

Assuming that Ram got the job at 25, by this time his age is 35. He is still young and has a growing portfolio of more than 13 lakhs in stock markets, plus he is now free to invest in guaranteed return schemes by the government. By now his salary is 1 lakh pm and he invests 25% of it in FDs giving a return of 6% a year.

Assuming that his salary increases, but he still is able to save only Rs. 25,000/- per month as his expenses have also increased.

Suppose his stock market returns are just 25% a year – here is the calculation of what he will get when he retires at 60 (calculated as Rs. 13,44,000/- giving an ROI of 25% a year for 35 years):

Well, it’s coming too much therefore I am not showing you the calculations. You can see for yourself here.

Ok, here is what he will get at retirement (age 60): Rs. 108,56,74,553.98 (One Hundred Eight Crores+)

Well that looks like too much, so let’s reduce it to 20% return a year (calculated as Rs. 13,44,000/- giving an ROI of 20% a year for 35 years):

Future Value: Rs. 31,90,33,765.75 (Rs. 31 Crores 90 Lakh+)

Did you notice even 20% a year will fetch you amazing returns – then what is the need to try 10% a month which is equal to 120% a year? Making 10% a month for a long time in stock markets is simply impossible.

Now here is what he will get from his fixed deposits:

Here is the calculation for Rs. 25,000/- deposit every month for 25 years giving an ROI of 6% a year:

Final investment value: Rs. 1,70,96,817.59 (Rs. One Crore 70 Lakh+)

Total interest earned: Rs. 95,71,817.59 (Rs. 95 Lakh+)

Total monthly deposits: Rs. 75,00,000.00 (Rs. 75 Lakh+)

Effective Annual Rate: 6%

Even 6% is a good return.

Total at retirement Ram will get:

31,90,33,765.75 + 1,70,96,817.59 = Rs. 33,61,30,583.34 (Rs. 33 Crores +)

Isn’t that enough money to fulfill all financial goals and live a great retired life even in 2050?

Do not forget that Ram was still living a good life when he had an average paying job. By the time he was 40, he had a good income spread over many investment vehicles that he can withdraw to buy a car, home, and other expensive items without too much financial burden on him.

Can you see proper money management can help you live a good life? Assuming that his stock market returns turned negative or gave some loss when he was 60 and withdraw all the leftover money – still, he has over one crore 70 lakh rupees to live a comfortable retired life.

Hope this article will help you to plan your investments in stock markets wisely. Be very conservative with your trading and your story may be same as Ram in this article. I will be very happy if that happens. 🙂

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

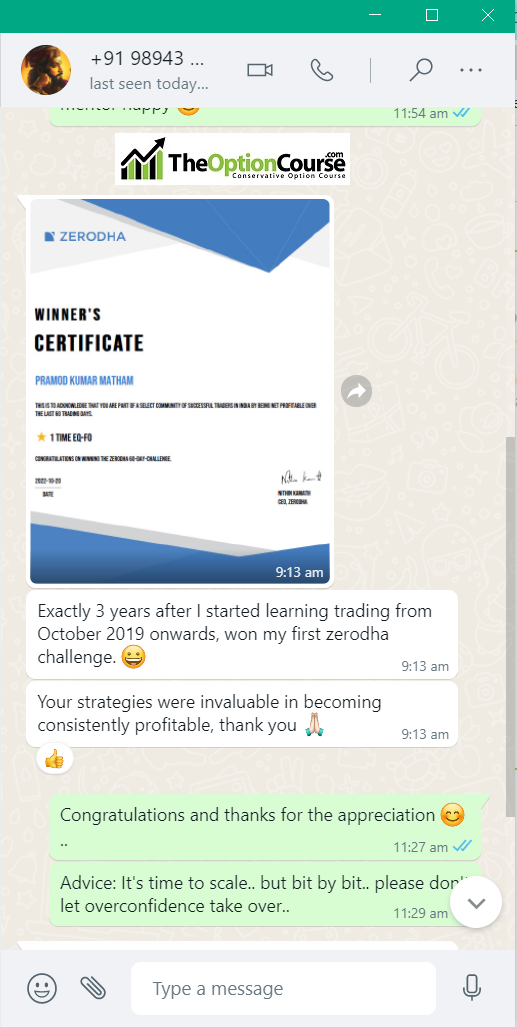

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users