Sponsored Ad: Click Here to Open a Share Trading Account Online for FREE and Pay ZERO Brokerage to Buy and Sell Shares!!!

Diwali 2023 is coming and you must be thinking what’s next? Here Are Some Simple Tips on Financial Management And Stock Investing

If you have done my course please continue trading options or futures with a hedge. If you have not done I suggest doing my course.

Here Are Some Simple Tips on Financial Management And Stock Investing You Can Follow:

- Avoid muhurat trading. In a short time, there is nothing you can do.

- If you still want to trade buy a good stock. Do not over-buy just because it’s Diwali. Do your research and invest.

- If you are a buyer of options kindly trade only intraday. Overnight options buying is dangerous as theta (time) decay will work against you even if you are right in the direction.

- If you are a seller of options or a future trade please hedge.

- Lastly, keep 5% of the margin blocked for the trade as a stop loss. Do not let the loss go beyond 5% of the margin. The target should be slightly above 5% – anything between 7.5 to 10% is good.

- Do not put more than 10% of your annual income into derivatives trading. This will keep your finances in check.

- Returning to No. 6 – if three years of your investment in derivatives trading (totalling 30% of three years of income) gives a negative return (you made losses) or is not above 12% return Year-Over-Year (YOY) then quit trading derivatives altogether.

- 20% of your annual income should go into stock investments. You can choose to divide this into mutual funds or direct investing. The best is 75% and 25%. 75% going into mutual funds and the remaining 25% into direct stock or ETF investing.

For example, if your take-home salary is 50,000 a month then 20% of 50k is 10,000. 75% of 10,000 is 7500 and the rest 25% is 2500. You can invest 7500 in Four good and diversified mutual funds and 2500 directly in stocks. Stock investing via SIP is also a good idea to average out the price. Do not invest in more than 5-10 stocks otherwise managing them may be a problem.

- If you keep doing point 8 above for 20 years then even at a 15% return compounded annually the total corpus will be:

Future investment value: ₹1,31,38,389.47

Total interest earned: ₹1,07,38,389.47

Total Deposits: ₹24,00,000.00

Time-weighted rate of return: 1269.27%

Suppose you started doing this at the age of 30, then by the time you are 50 years old, you will have enough to retire – all this by just investing 10k a month. Of course, with experience your salary will increase and you can invest more. I have not taken this into account. I assume this can go up to 2 crores of corpus by the time you are 50.

Follow the above rules and you will be a happy investor.

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

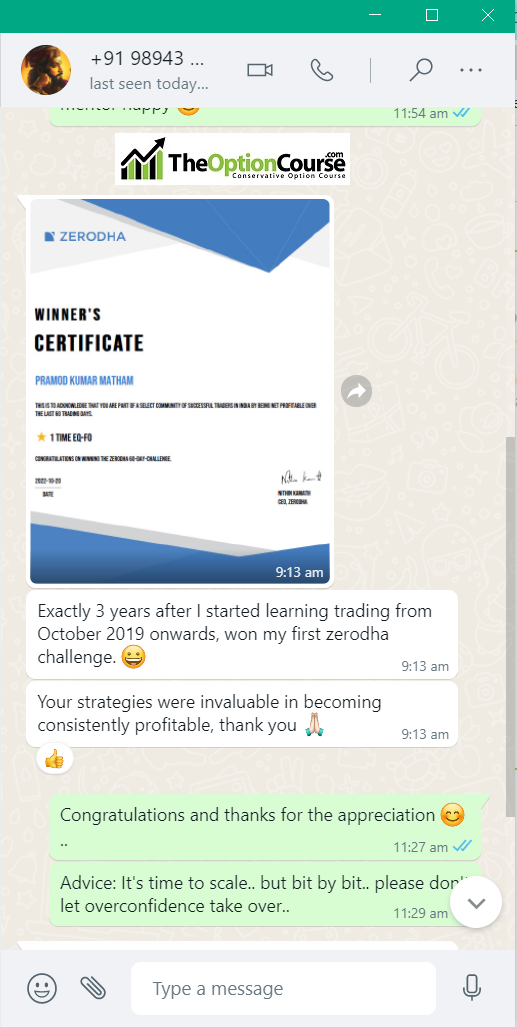

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users